Employees Provident Fund: Understanding How EPF helps you save on Tax in India?

- September 22, 2023

- Income Tax

Wondering How EPF helps you save on Tax in India? Many people think about how the working of the EPF takes place, EPF Being a tax-saving instrument acts as the cornerstone of the financial security of employees all around the country. EPF is one of the retirement savings schemes which not only ensures financial security to the individual but also provides several tax benefits. In this article, we will discuss about Working of the EPF Scheme and EPF taxation and also discuss that how EPF helps you save on Tax in India.

However, before we move on to find out how EPF helps you save on Tax in India, it is equally important to have a basic idea of what EPF or Employees Provident Fund is all about.

Table of Content

Meaning of Employees Provident Fund or EPF

The EPF Scheme or the Employees Provident Fund (EPF) is one of the initiatives of the government of India to financial security to the employees for their betterment at the time of their retirement. The Employees Provident Fund (EPF) finds its authority from the statutes known as the Employees’ Provident Funds and Miscellaneous Provisions Act, of 1952. The EPF Scheme is governed by the authority known as the Employees’ Provident Fund Organization (EPFO). EPF applies to all establishments that have a minimum of 20 workers and are engaged in industries as specified by the government.

The EPF is a contributory fund where both the employee and the employer make monthly contributions. The EPF fund gets accumulated over the years, and employees can access the funds upon retirement, resignation, or other specified circumstances.

Also read our Article on: All about Employees Provident Fund (EPF)

How does EPF help you save on tax in India?

These are the situations in which EPF helps you in saving your tax liabilities:

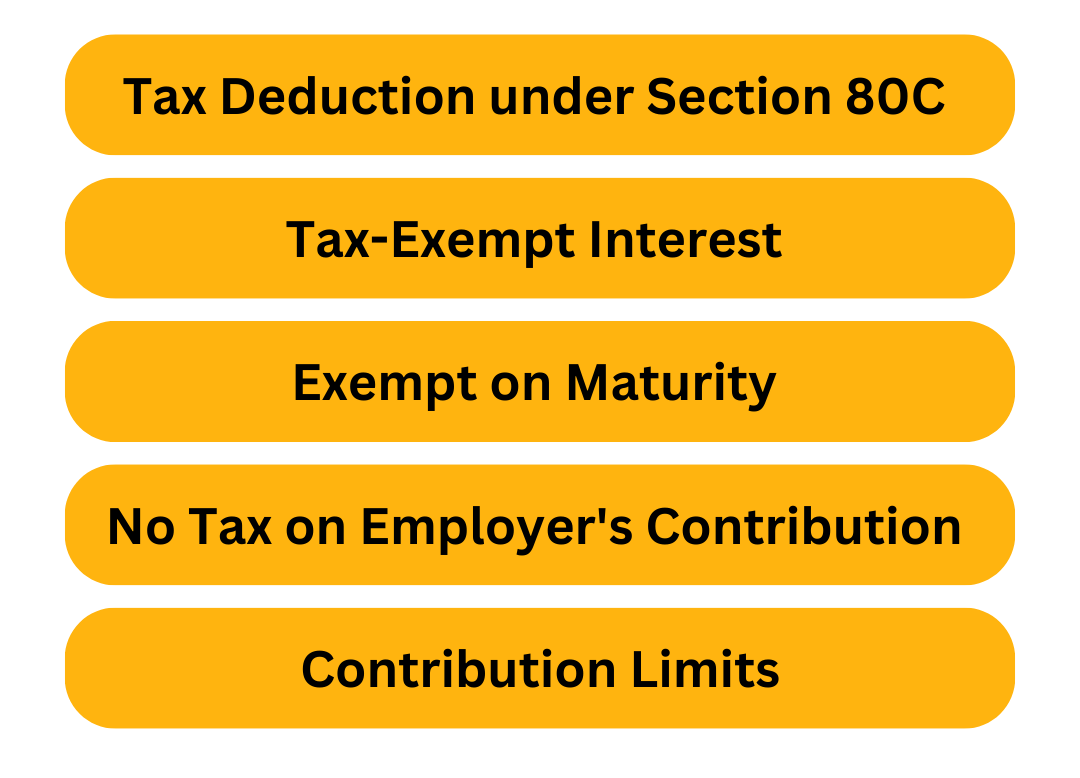

- Tax Deduction under Section 80C: One of the significant benefits of contributing to the EPF is the EPF 80C deduction available under Section 80C of the Income Tax Act, of 1961. EPF under 80C of the Income Tax Act, 1961, states that the contributions are made by the employee is the EPF is allowed to claim the deduction up to a maximum limit of Rs. 1.5 lakh which can be claimed later by the employee on filing an Income Tax Return.

- Interest Earned is Tax-Exempt : The interest earned on the EPF contributions is tax-exempt. The interest rate is declared by the government each year and is often competitive compared to other investment options. This makes EPF an attractive investment avenue for those seeking a safe and tax-efficient way to grow their savings.

- Exempt on Maturity : The accumulated corpus in the EPF account, including the principal amount and interest earned, is tax-free at the time of maturity or withdrawal. This is applicable when the employee completes five continuous years of service, making the EPF an excellent tool for long-term wealth creation.

- No Tax on Employer’s Contribution : The employer’s contributions to the EPF Scheme do not take the form of taxable income for the employee. This factor provides an additional advantage to the employee as the employee is not obliged to include the contribution made by the employer in their taxable income.

- Contribution Limits: Employees who have registered themselves in EPF can contribute to their choice in the scheme as there are no upper limits on the contribution made by the employee to the EPF. On the other hand, the employer’s contribution power is limited to up to 12% of the Basic Salary and Dearness Allowance of the Employee.

Advantages of Employees Provident Fund (EPF) in India

The key benefits and advantages of the Employees Provident Fund in India are:

- Retirement Savings and Financial Security: One of the primary advantages of the EPF is its role in ensuring retirement savings and financial security for employees. By contributing a portion of their salary to the EPF throughout their working years, employees build a substantial corpus that can be accessed upon retirement. This fund serves as a reliable source of income after an individual’s active earning years, providing a sense of financial stability during the golden years.

- Employer Contribution: The EPF is characterized by dual contributions—both the employee and the employer contribute to the fund. This unique feature ensures that the burden of building a retirement fund is shared between the employer and the employee. The employer’s contribution enhances the overall savings and provides an added incentive for employees to participate actively in the scheme.

- Tax Benefits: EPF contributions offer attractive tax benefits to both employees and employers. Employee contributions are eligible for tax deductions under Section 80C of the Income Tax Act, 1961 up to a specified limit. Moreover, the interest earned on EPF contributions is tax-free, making it an efficient way to accumulate wealth over time. Employers also benefit from tax exemptions on their contributions, making the EPF a tax-efficient investment scheme.

- Compounding Interest: The EPF offers compounded interest on the accumulated corpus, which has a compounding effect on the overall savings. Over the years, compounding allows the fund to grow substantially, maximizing the returns for employees. The power of compounding ensures that even small, regular contributions can lead to a significant sum at retirement.

- Loan and Withdrawal Facilities: In addition to retirement benefits, the EPF scheme provides provisions for partial withdrawals and loans for specific purposes such as medical emergencies, housing needs, education, and marriage. These options provide employees with financial flexibility during critical life stages, without compromising their long-term savings goals.

Employee Provident Fund Interest Rate for FY 2023–2024

As per the approval of the Union Ministry for Labour and Employment, for the Financial Year 2023–2024, the EPF scheme will be receiving interest at a rate of 8.15 percent.

As per the guideline issued by the Employees’ Provident Fund Organisation (EPFO) dated, 24th July, the Central Government has given the authority to the labor ministry to credit interest at a rate of 8.15% annually for 2021–2022 to every individual who has opted for EPF program.

The circular also directs the relevant authorities to give the required directives for crediting interest to EPF members’ accounts.

The 8.15 percent interest rate on provident funds for this fiscal year was decided by the Central Board of Trustees (CBT) of the EPFO on March 28.

The CBDT suggested adding protections to the amount that balanced the growth and surplus funds. The 8.15 percent proposed interest rate provides higher revenue for members while protecting the surplus. Both the interest rate (8.15%) and the surplus of Rs 663.91 crore are greater than they were the previous year.

Reasons to Choose EPF in India

The following are the reasons to choose the Employee Provident Fund (EPF) Scheme:

- Retirement Security: EPF ensures a stable financial future by building a corpus for your retirement. Regular contributions from both employee and employer accumulate over the years, providing a reliable source of income post-retirement.

- Employee Benefits: EPF offers attractive interest rates, often higher than traditional savings accounts. This ensures that your savings grow steadily, safeguarding against inflation and economic fluctuations.

- Tax Benefits: EPF contributions are eligible for tax deductions under Section 80C of the Income Tax Act. This dual advantage of saving for retirement while reducing your taxable income is a compelling reason to choose EPF.

- Employer Contribution: Employers also contribute to your EPF account, effectively boosting your retirement savings without any additional effort or cost on your part.

- Long-Term Savings Habit: EPF instills a disciplined savings habit. The mandatory contribution encourages individuals to save consistently, promoting financial prudence.

- Partial Withdrawals: EPF allows for partial withdrawals for specific purposes like education, medical emergencies, and home purchases, ensuring a safety net during unforeseen circumstances.

- Social Security Net: EPF provides a social security net to employees, ensuring financial stability not only for the account holder but also for their family.

- Low Risk: EPF is a low-risk investment avenue as it is managed by the government. It offers a reliable, stable, and secure way to grow your savings.

- Universal Accessibility: EPF is accessible across India and its vast network ensures ease of operation even if you switch jobs.

- Simplicity: The EPF process is straightforward. Both employees and employers can contribute easily through automated processes, reducing administrative hassles.

Employee Provident Fund (EPF): Your Perfect Retirement Plan in India

When you think of your retirement EPF may come into mind. EPF indeed is a very good option for your retirement. EPF is a form of tax saving instrument in which some amount of money is deducted every month from the individual’s salary and is saved in the EPF Account.

Over time, this money grows with interest. When you retire, you’ll have a substantial fund waiting for you.

EPF offers several benefits. First, it’s a disciplined way to save for the future. Second, the contributions and interest enjoy tax benefits. Plus, the EPF interest rates have historically been competitive.

Accessing the money isn’t difficult either. You can withdraw the EPF corpus at retirement or even during emergencies like medical expenses. With recent online services, managing your EPF account is easier than ever.

For EPF Registration, Please Read: Difference between EPF, GPF And PPF: Registration Process For EPF

Takeaway

The Employee Provident Fund (EPF) is not only a valuable savings tool for retirement but also a potent instrument for tax saving in India. Its EEE status, deductions under Section 80C, and tax-free withdrawals after 5 years make it an attractive option for employees. Employers also benefit from tax deductions on their contributions. However, it’s crucial to understand the rules and regulations governing EPF contributions and withdrawals to make the most of its tax-saving benefits. Hope you understand that how EPF helps you save on Tax in India.

As tax laws can change over time, it’s advisable to consult a financial expert or tax advisor for the most up-to-date information and personalized advice; you can connect with our Tax Experts at Legal Window for more information regarding the Benefits and Applicability of EPF.

CA Pulkit Goyal, is a fellow member of the Institute of Chartered Accountants of India (ICAI) having 10 years of experience in the profession of Chartered Accountancy and thorough understanding of the corporate as well as non-corporate entities taxation system. His core area of practice is foreign company taxation which has given him an edge in analytical thinking & executing assignments with a unique perspective. He has worked as a consultant with professionally managed corporates. He has experience of writing in different areas and keep at pace with the latest changes and analyze the different implications of various provisions of the act.

Categories

- Agreement Drafting (23)

- Annual Compliance (11)

- Change in Business (36)

- Company Law (148)

- Compliance (90)

- Digital Banking (3)

- Drug License (3)

- FEMA (17)

- Finance Company (42)

- Foreign Taxation (6)

- FSSAI License/Registration (14)

- GST (118)

- Hallmark Registration (1)

- Income Tax (200)

- Latest News (34)

- Miscellaneous (164)

- NBFC Registration (8)

- NGO (14)

- SEBI Registration (6)

- Section 8 Company (7)

- Start and manage a business (21)

- Startup/ Registration (128)

- Trademark Registration/IPR (40)

Recent Posts

- Post incorporation compliances for companies in India April 30, 2024

- Startup’s Guide to Employee Stock Ownership Plans April 29, 2024

- Master Secretarial Audit: A Complete Compliance Guide April 27, 2024

About us

LegalWindow.in is a professional technology driven platform of multidisciplined experts like CA/CS/Lawyers spanning with an aim to provide concrete solution to individuals, start-ups and other business organisation by maximising their growth at an affordable cost.

Ask an Expert

")

")

")

in NBFC Risk Management (1)")

")

")