Old vs. New Tax Regime in India: A Comprehensive Comparison

- September 2, 2023

- Income Tax

The Indian taxation regime has undergone a significant transformation with the introduction of the New Tax Regime (NTR) alongside the pre-existing Old Tax Regime (OTR). This move was aimed at providing taxpayers with more flexibility and options when it comes to choosing the tax regime that best suits their financial situation. The choice between these two regimes has sparked debates and discussions among taxpayers and experts, each having its own set of advantages and disadvantages. In this article, we will delve into the key differences and considerations between the Old vs New Tax regime in India.

Let us discuss the Old Tax Regime and the New Tax Regime in detail before we move on to discuss about difference between old and new tax regime and to discuss which one to opt from new vs old regime.

Old Tax Regime in India

The Old Tax Regime, as laid out in the Income Tax Act, 1961, was the traditional method of calculating and paying income tax. It involves a systematic approach to computing taxable income, allowing for deductions and exemptions based on various factors like investments, expenses, and eligible allowances. Taxpayers availing of the old tax regime follow a structure where they can claim a multitude of deductions under various sections of the Income Tax Act, which ultimately reduce their taxable income and consequently, their tax liability.

Provisions and Implications regarding Old Tax Regime

The following are the Provisions and Tax Implications concerning Old Tax Regime:

- Deductions and Exemptions: Under the old tax regime, taxpayers are eligible to claim deductions and exemptions allowed under specific sections of the Income Tax Act. These include deductions for investments made in instruments like Public Provident Fund (PPF), National Savings Certificates (NSC), tax-saving fixed deposits, and more. Additionally, exemptions such as House Rent Allowance (HRA), Leave Travel Allowance (LTA), and others can be availed, reducing the taxable income.

- Income Slabs and Tax Rates: The old tax regime features a progressive tax structure, where individuals are divided into different income slabs, and each slab is subject to a specific tax rate.

- Specific Provisions for Senior Citizens and Very Senior Citizens: The old tax regime offers additional benefits to senior citizens and very senior citizens through higher exemption limits and lower tax rates in certain cases.

- Investment-Focused Approach: The old tax regime encourages investments in various financial instruments, real estate, and other avenues that are eligible for deductions. This approach is aimed at promoting savings and investment habits among taxpayers.

Understanding the New Tax Regime

Under the New Tax Regime, taxpayers have the option to choose between the existing tax structure with deductions and exemptions or the new structure with reduced tax rates and limited deductions. The new regime introduces lower tax rates, which vary according to the taxpayer’s income slab. The objective is to simplify the tax calculation process and reduce the compliance burden on taxpayers.

Key Features of the New Tax Regime

The following are the key Features of New Tax Regime:

- Reduced Tax Rates: The new tax regime offers lower tax rates compared to the existing regime, effectively reducing the tax liability for many taxpayers. The reduced rates aim to incentivize individuals to opt for this new structure.

- No Deductions and Exemptions: One of the notable differences between the two regimes is the absence of various deductions and exemptions in the new regime. Taxpayers who choose the new regime will not be able to claim deductions under sections such as 80C, 80D, and 24(b), among others.

- Simplified Tax Calculation: The new regime follows a simplified tax calculation process, which can be advantageous for taxpayers who find the existing regime’s calculations complex and time-consuming.

- Optional Choice: Taxpayers have the flexibility to choose between the existing tax regime and the new regime, based on their individual financial situations and preferences. This ensures that taxpayers can select the option that best suits their needs.

Income Tax Slab Rates for the New vs. the Old Tax Regime

The following are the tax slab rates for the New vs. the Old Regime:

Simply put, under the new regime, income between Rs. 6 lakh and Rs. 9 lakh is subject to a 10% tax rate while income between Rs. 9 lakh and Rs. 12 lakh is subject to a 15% tax rate. According to the budget statement for 2023, if the total income is less than Rs 7 lakh, the tax refund is enhanced to for the new tax regime. Additionally, the standard deduction is now accessible under the new tax regime.

Consideration of deductions and exemptions that must be kept in mind when choosing a New Tax Regime

The Act includes a number of exclusions and deductions, which the government is aware makes it difficult for taxpayers to comply with the legislation and for the tax authorities to administer it.

Specific tax deductions and exemptions must be given up in order to implement the streamlined new tax rate regime and provide assistance to taxpayers. Therefore, it’s crucial to balance the impact of claimed deductions and exemptions against the advantage of lower tax rates. Popular tax deductions and exemptions that are no longer permitted under the new tax regime include:

- LTA: Leave Travel Allowance

- The HRA, or house rent allowance

- Child tuition assistance

- Tax-related professional deductions

- Interest on a mortgage

- Deduction for certain purchases or costs under Chapter VI-A, including:

- Deductions under Section 80C can be made for contributions to the public provident fund, mortgage principal repayment, child care costs, life insurance premiums, etc.

- Extra deductions for health insurance premiums, student loan interest, etc.

Old vs. New Tax Regime: Choosing the Suitable Tax Regime

Depending on their unique situation and income sources, an individual or HUF taxpayer may choose the new tax regime. You have the option of switching from the old to the new tax regime every year or just once. However, the frequency is largely influenced by the annual source of money.

- When money comes from a Job or a Business

Once the option to take advantage of new tax rates for a financial year has been exercised, the new rates shall apply for succeeding years in the situation where an individual or HUF obtains income from a business or profession. In the event that their circumstances change, the law gives such taxpayers a single choice to return to the previous tax regime. In the absence of the taxpayer ceasing to receive any income from a business or profession, this switch-back option is only accessible once in a taxpayer’s lifetime.

- If money does not come from a Job or a Business

The decision may be made annually if an individual or HUF does not have revenue from a business or profession. Employers are required to withhold tax from employees’ paychecks prior to paying them. However, the employee must let the employer know what tax rates they desire.

An employee has the option to select between the old and new tax regimes at the start of the year and to notify their employer, as well as when they begin a new job during the year. The employee can, however, alter the tax regime while completing the personal tax return.

For instance, if an employee chooses the new tax regime at the beginning of the year, the employer will withhold tax based on the new tax regime slab rates. However, they make some tax-deductible investments during the year, such as paying provident fund contributions and medical insurance premiums, and when it comes time to filing income tax returns (ITR); they find the old tax regime is better for them. In this case, even though the employer had withheld taxes based on the new tax regime, they had the option of choosing the old tax regime when filing their tax return.

Old vs. New Tax Regime: Which is better Old Regime Vs. New Regime?

With the new tax regime’s modifications and an individual with an annual income of INR 9 lakh will pay INR 45,000 in tax, which is 5% of the salary, a reduction of INR 15,000 from the current INR 60,000 under the previous slabs under the new tax regime. In addition, an individual earning INR 15 lakh per year will pay INR 1.5 lakh in tax, down from INR 1.87 lakh.

However, if the individual is entitled to claim deductions/exemptions under the previous tax regime for HRA, LTA, PPF, and so on, the old tax regime may be more beneficial.

Because the allowed deductions, sources, and amount of income vary by individual, one rule cannot be applied to all. Taxpayers must examine and compare their tax burden under both regimes before deciding which to use.

If a taxpayer has investments in tax-saving instruments, pays premiums on life or medical insurance policies, children’s school fees, home loan principal repayment, and so on, and takes advantage of the deduction for HRA, LTA, and so on, it may be more advantageous to opt for the old tax regime because the benefit of deduction/exemption can be taken advantage of in the old tax regime.

The new tax regime allows a standard deduction of INR 50,000 for salaried individuals and a deduction for family pensions of INR 15,000 or one-third of the pension.

Example of Income Tax Calculation (Old vs. New Tax Regime)

Let us understand which tax regime is better option for tax payers through an illustration explaining with the help of Tabular Representation of choosing between New Vs Old Regime.

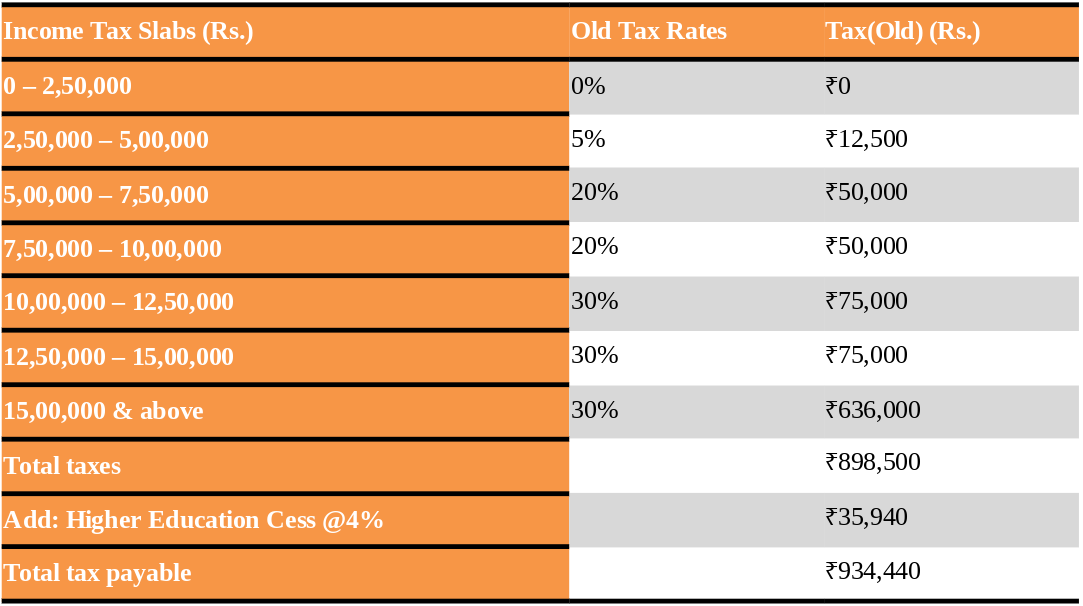

- Old vs New Tax Regime: Total Tax Payable as per Old Tax Regime

If a Taxpayer chooses to opt for Old Tax Regime, he has to pay the as per the following:

- Old vs New Tax Regime: Total Tax Payable as per New Tax Regime

If a Taxpayer chooses to opt for New Tax Regime, he has to pay the as per the following:

So, as you can see, the new tax regime is better. By choosing the new tax regime over the old, you will save income tax of Rs 14,040 in taxes.

How to Continue with the Old Tax Regime in 2023?

Currently, a taxpayer with business or professional income must file Form 10IE in order to elect the new tax regime. This form will be available in October 2020.

According to the Union Budget 2023 modifications to the new tax regime, taxpayers will be forced to choose the old tax regime from FY 2023-24 onwards, with the new tax regime being the default choice.

The tax department will issue instructions on how to choose the old tax regime in due time.

Also Read our Article on: How to Calculate Income Tax for Salaried Individual?

Summing Up

Both the old and new tax slab has benefits and drawbacks. The taxpayer had many investment options due to the diversity of deductions and exemptions available under the old tax regime, such as PPF, ELSS, and Mediclaim. As their income has just recently begun, the new tax regime is suited to new investors and individuals who have only recently begun their careers.

As a result, the only method to establish which tax regime is preferable for you is to enter your income into both regimes in order to calculate the actual tax payable.

Connect with our Tax Experts at Legal Window, in case you also need an expert opinion on which tax regime would be suitable for you?

CA Pulkit Goyal, is a fellow member of the Institute of Chartered Accountants of India (ICAI) having 10 years of experience in the profession of Chartered Accountancy and thorough understanding of the corporate as well as non-corporate entities taxation system. His core area of practice is foreign company taxation which has given him an edge in analytical thinking & executing assignments with a unique perspective. He has worked as a consultant with professionally managed corporates. He has experience of writing in different areas and keep at pace with the latest changes and analyze the different implications of various provisions of the act.

Categories

- Agreement Drafting (23)

- Annual Compliance (11)

- Change in Business (36)

- Company Law (148)

- Compliance (90)

- Digital Banking (3)

- Drug License (3)

- FEMA (17)

- Finance Company (42)

- Foreign Taxation (6)

- FSSAI License/Registration (14)

- GST (118)

- Hallmark Registration (1)

- Income Tax (200)

- Latest News (34)

- Miscellaneous (164)

- NBFC Registration (8)

- NGO (14)

- SEBI Registration (6)

- Section 8 Company (7)

- Start and manage a business (21)

- Startup/ Registration (128)

- Trademark Registration/IPR (40)

Recent Posts

- Post incorporation compliances for companies in India April 30, 2024

- Startup’s Guide to Employee Stock Ownership Plans April 29, 2024

- Master Secretarial Audit: A Complete Compliance Guide April 27, 2024

About us

LegalWindow.in is a professional technology driven platform of multidisciplined experts like CA/CS/Lawyers spanning with an aim to provide concrete solution to individuals, start-ups and other business organisation by maximising their growth at an affordable cost.

Ask an Expert

")

")

")

in NBFC Risk Management (1)")

")

")